Macroeconomic and industry conditions Business environment

In October 2022, the International Monetary Fund (IMF) again lowered its forecast for global growth for 2022, referring to a fundamental change in the global economy, which has now become more unpredictable, more volatile and more exposed to geopolitical tensions. Europe is particularly affected by the consequences of the Russian attack on Ukraine, while high inflation is weighing on consumer confidence in the United States and the pandemic-related restrictions are continuing to place a damper on the corporate sector in China. At the end of January 2023, the IMF updated its growth forecast, as the global economy is coping with the consequences of the war in Ukraine and the continued high inflation somewhat better than initially feared.

It now projects an increase of 3.4% in global gross domestic product. As a result, the Eurozone expanded by 3.5%, thus also exceeding the forecast; with growth of 1.9%, Germany performed significantly better than initially expected but is lagging behind its European peers. India (+6.8%) and the ASEAN countries (+5.3%) achieved the greatest growth rates. At 3.0%, growth in China was slightly slower than originally expected.

The German Mechanical and Plant Engineering Association (VDMA) stated in February 2023 that despite the challenging macroeconomic conditions the mechanical engineering industry had proved resilient in many segments in 2022 and that in many cases the third quarter had even seen stronger production growth than expected following the easing of the supply chain constraints for some intermediate products. However, it cautioned that the shortage of electronic components was still clearly being felt by many companies, adding that revenue in the fourth quarter of 2022 had been weak at the large mechanical engineering sites outside the EU-27.

According to initial figures from the German Federal Statistical Office, production output in the mechanical and plant engineering sector in Germany exceeded the previous year by 0.2% in real terms in 2022. [This is a preliminary figure and subject to change]. This directly reflects global challenges such as the war in Ukraine, supply chain bottlenecks, high energy prices and inflation. In addition, preventive measures to stem the Covid-19 pandemic resulted in far-reaching restrictions on public life in China. The employment market remained resilient. However, the shortage of skilled workers prevented the completion of machinery, machine parts and components in many cases. Many companies would like to hire new staff in response to the high order backlog. However, finding qualified employees is proving to be difficult. It is not only skilled workers that are scarce, but employees in their entirety, according to the VDMA.

Year-on-year gross domestic product (%)

| Country/region | 2020 | 2021 | 2022 (Estimate) |

| World | -3.0 | 6.2 | 3.4 |

| Developed economies | -4.4 | 5.4 | 2.7 |

| Eurozone | -6.1 | 5.3 | 3.5 |

| Germany | -3.7 | 2.6 | 1.9 |

| France | -7.9 | 6.8 | 2.6 |

| Italy | -9 | 6.7 | 3.9 |

| Spain | -10.8 | 5.5 | 5.2 |

| United Kingdom | -9.3 | 7.6 | 4.1 |

| USA | -3.4 | 5.9 | 2.0 |

| Japan | -4.6 | 2.1 | 1.4 |

| Emerging markets and developing countries | -1.9 | 6.7 | 3.9 |

| ASEAN* | -3.4 | 3.8 | 5.2 |

| Brazil | -3.9 | 5 | 3.1 |

| China | 2.2 | 8.4 | 3.0 |

| India** | -6.6 | 8.7 | 6.8 |

| Russia | -2.7 | 4.7 | -2.2 |

**) Fiscal year from 1 April to 31 March

Source: IMF World Economic Outlook Update January 2023, for 2020: IMF October 2022 Database.

Business performance

Overall statement on business performance

The Koenig & Bauer Group’s business performance in 2022 was adversely affected by global macroeconomic trends. The war in Ukraine with its consequences for energy prices, inflation and interest rates as well as worldwide supply bottlenecks took their toll. The impact of the Covid-19 pandemic also exerted pressure on business outside China in the first few months of the year, after which it was combined almost solely to China. The massive rise in some raw material and energy prices also led to higher material costs in 2022, which it was only possible to pass on in part and with a delayed effect by increasing prices.

However, the Koenig & Bauer Group took extensive precautions at an early stage to prepare for the challenging situation. In 2022, the Company again worked successfully on the P24x efficiency programme, which had been adopted in September 2020. The accelerated implementation of the programme yielded savings of around €92m as of 31 December 2022. This was particularly spurred by measures aimed at boosting the Group’s productivity as well as adjustments to capacities and lower quality assurance expenses. Furthermore, successful negotiations with suppliers and the optimised use of cash discounts resulted in significant purchasing benefits, which also fundamentally offset the recent price increases. Further potential was leveraged in R&D, e.g. through the series start-up of selected presses. In response to the capacity utilisation shortfalls caused by supply chain constraints, short-time working was also utilised to a minor extent in 2022 at three locations in addition to flexible working hours.

To strengthen the Group’s stability and strategic flexibility, the Company obtained a flexibly repayable KfW loan of up to €120m in November 2020 to supplement the existing syndicated credit facilities. As no dividend distributions are permitted during the term of the KfW loan, the Management Board and the Supervisory Board will be proposing to the Annual General Meeting that the net profit achieved by the holding company Koenig & Bauer AG be retained. For this reason, the Company aims to discharge the KfW loan as quickly as possible so that dividend distributions can be resumed. Financially, the Koenig & Bauer Group is well positioned, with a Group equity ratio of roughly 29.2% (previous year: 28.7%) and more than €250m in freely available cash and cash equivalents. This was also aided by active net working capital management in the year under review.

Group order backlog

| €m | 2021 | 2022 |

| Sheetfed | 441.6 | 582.9 |

| Digital & Webfed | 88.5 | 112.3 |

| Special | 277.6 | 253.4 |

| Überleitung | -0.9 | 1.8 |

| Gesamt | 806.8 | 950.4 |

Group order intake

| €m | 2021 | 2022 |

| Sheetfed | 751.9 | 813.5 |

| Digital & Webfed | 142.3 | 163.6 |

| Special | 430.4 | 392.9 |

| Überleitung | -34.0 | -40.7 |

| Gesamt | 1,290.6 | 1,329.3 |

Operating earnings continued to improve from quarter to quarter in 2022. At €950.4m at the end of December, the order backlog was high, also compared to previous years. The following picture emerged in the individual segments: While Sheetfed was already able to achieve further growth in order intake in the first half of the year after a very strong fourth quarter in 2021, the Digital & Webfed segment posted an increase in the final quarter of 2022. The Special segment, however, displayed a steady increase in order intake up to the third quarter of 2022. Group order intake amounted to €1.33bn at the end of 2022 (previous year: €1.29bn), thus meeting expectations. The book-to-bill ratio of 0.8 in the fourth quarter was in line with the Company’s own forecast. The Koenig & Bauer Group generated revenue – equivalent to operating revenue – of €1,185.7m in 2022 (2021: €1,115.8m) and consolidated earnings before interest and taxes (EBIT) – equivalent to operating EBIT – of €22.0m (2021: €28.5m). The EBIT margin of 1.9% (2021: 2.6%) thus achieved corresponds to the operating EBIT margin. The reason for this definition is that special effects of around €23m net had arisen in the previous year as a result of the adjustment to the restructuring provisions for the P24x efficiency programme. There were no special effects in the year under review.

The segments contributed the following revenue in 2022: Sheetfed €672.2m (2021: €642.4m); Digital & Webfed €139.8m (2021: €121.4m), Special €417.1m (2021: €390.2m). At €1,185.7m, Group revenue was therefore at the upper end of the Company’s own forecast of €1,160 – 1,190m, as stated in November. The segments contributed the following EBIT in the year under review: Sheetfed €19.0m (2021: €24.0m); Digital & Webfed €–19.3m (2021: €–38.5m), Special €23.2m (2021: €34.9m). The original forecast had assumed a slight increase over the previous year for Group revenue (2021: €1,115.8m) and for the EBIT margin (2021: 0.5%). As a result of the aforementioned special effects occurring in 2021, the Sheetfed and Special segments were down on the previous year, as EBIT had been inflated by the adjustment of the restructuring provisions for P24x by around €9m in the Sheetfed segment and by around €18m in the Special segment. The Digital & Webfed segment, on the other hand, performed better than in the previous year, as EBIT had been roughly €6m lower due to the adjustment to the restructuring provisions for P24x in the previous year. At €22.0m, corresponding to an EBIT margin of 1.9%, EBIT exceeded the Company’s own forecast of €15 – 20m (EBIT margin between 1.3% and 1.7%) and market expectations.

To summarise, the Koenig & Bauer Group’s business performance and business situation in 2022 were better than expected given the prevailing global challenges.

Earnings

At the end 2022, the Koenig Bauer & Group’s order intake came to €1,329.3m, up 3.0% on the already good figure of €1,290.6m reported in the previous year. At €1,185.7m, Group revenue exceeded the previous year’s figure by 6.3%. As in the previous year, almost 30% of revenue was generated from service business in 2022. The Group export ratio widened from 86.2% to 88.6%, with the proportion of business coming from Europe excluding Germany growing to 34.9% (previous year: 32.6%), while the share of North American business also expanded to 20.5% (previous year: 15.8%). The share of revenue coming from Germany (11.4%), Asia/Pacific (24.1%) and Latin America and Africa (9.1%) was down on the previous year (13.8%, 26.0% and 11.8%, respectively).

Gross profit increased to €317.4m (previous year: €298.1m) despite the higher production costs. The gross margin widened slightly to 26.8% (previous year: 26.7%), also due to the effects of P24x. At €54.2m (previous year: €46.7m), R&D expenses were up on the previous year, mainly due to the higher depreciation and amortisation of development costs. Selling expenses rose to €147.3m (previous year: €131.1m) primarily as a result of elevated freight, travel and advertising costs. Administrative expenses also climbed by €4.4m over the previous year due to the increase in Group amortisation and depreciation expense as well as higher personnel expenses, amounting to €92.8m (previous year: €88.4m). Net other expenses came to €–0.6m, compared with €–4.4m in the previous year. Among other things, this was due to currency-translation effects. All told, this resulted in EBIT of €22.0m (previous year: €28.5m), equivalent to an EBIT margin of 1.9%, down from 2.6% in the previous year.

The improvement in operating earnings over the previous year is mainly due to the P24x efficiency programme (roughly €30m) despite the lower use of short-time work in the previous year (roughly €8m), positive volume and mix effects (roughly €19m) and other negative effects that also include loss allowances on receivables and currency-translation effects (roughly €14m). The effects of higher cost of materials and energy (around €31m) were not fully offset by the announced price increases (roughly €21m). This is primarily due to the time lag in the third and fourth quarters of 2022 in particular between price increases and cost increases, for example in connection with energy costs and electronic components.

The net interest expense of €8.8m (€9.5m) was slightly lower than in the previous year, resulting in earnings before taxes of €13.2m (previous year: €19.0m). After income taxes, the Group posted net profit of €11.1m in 2022 (previous year: €14.5m). This translates into earnings per share of €0.63 (previous year: €0.83).

Group revenue

| €m | 2021 | 2022 |

| Sheetfed | 642.4 | 672.2 |

| Digital & Webfed | 121.4 | 139.8 |

| Special | 390.2 | 417.1 |

| Reconciliation | -38.2 | -43.4 |

| Total | 1,115.8 | 1,185.7 |

Group revenue by product group

| €m | 2021 | 2022 |

| Service | 329.8 | 353.7 |

| Printing presses | 774.3 | 821.3 |

| Other | 11.7 | 10.7 |

Group revenue by regions

| €m | 2021 | 2022 |

| Germany | 153.8 | 134.7 |

| Rest of Europe | 364.4 | 414.4 |

| North America | 176.7 | 243.4 |

| Asia/Pacific | 289.6 | 286.1 |

| Africa/Latin America | 131.3 | 107.1 |

| Total | 1,115.8 | 1,185.7 |

| % | ||

| Germany | 13.8 | 11.4 |

| Rest of Europe | 32.6 | 34.9 |

| North America | 15.8 | 20.5 |

| Asia/Pacific | 26.0 | 24.1 |

| Africa/Latin America | 11.8 | 9.1 |

Group income statement

| €m | 2021 | 2022 |

| Revenue | 1,115.8 | 1,185.7 |

| Cost of sales | -817.7 | -868.3 |

| Gross profit | 298.1 | 317.4 |

| Research and development costs | -46.7 | -54.2 |

| Selling costs | -131.1 | -147.3 |

| Administrative costs | -88.4 | -92.8 |

| Other operating income/expenses | -4.4 | -0.6 |

| Remeasurement gains and losses | 0.9 | 0.3 |

| Other financial result | 0.1 | -0.8 |

| Earnings before interest and taxes (EBIT) | 28.5 | 22.0 |

| Interest result | -9.5 | -8.8 |

| Earnings before taxes (EBT) | 19.0 | 13.2 |

| Income taxes | -4.5 | -2.1 |

| Group profit | 14.5 | 11.1 |

| Earnings per share | 0.83 | 0.63 |

| % of revenue | 2021 | 2022 |

| Cost of sales | -73.3 | -73.2 |

| Research and development costs | -4.2 | -4.6 |

| Selling costs | -11.7 | -12.4 |

| Administrative costs | -7.9 | -7.8 |

| Other income/expenses | -0.4 | -0.1 |

| Interest result | -0.9 | -0.7 |

| Income taxes | -0.4 | -0.2 |

| Group profit | 1.3 | 0.9 |

Finances

Cash flow from operating activities fell from €95.0m in the previous year to €5.4m in the year under review, mainly due to increased inventories and trade receivables. The increased prepayments received had the opposite effect. Cash flow from investing activities, which also includes the acquisition of shares in Celmacch, thus changed from €–38.7m in the previous year to €–65.1m in the year under review. Free cash flow amounted to €–59.7m. The decrease of €116.0m in cash flow from operating activities was particularly due to changes in net working capital in addition to heightened investing activities. Cash flow from financing activities came to €59.4m (previous year: €–68.4m). In the previous year, the partial repayment of around €60m towards the syndicated loan had a substantially stronger effect than in the year under review (of around €6m). At the end of December 2022, cash and cash equivalents of €132.2m (previous year: €129.5m) were available. Adjusted for bank liabilities of €195.9m, net financial debt amounted to €–63.7m (previous year: €2.9m).

The Group has access to syndicated credit facilities of a total of €400m from a consortium of excellent banks. The syndicated finance, which consists of a guarantee credit facility and a revolving credit facility of €200m each, has a term expiring in December 2024. Against the backdrop of the Covid-19 pandemic and the related funding programmes, Koenig & Bauer was also able to reach an agreement with KfW and the syndicate banks in 2020 to increase the revolving credit facility by €120m on standard market terms in order to ensure the Company’s economic stability. This adjusted facility also has a term expiring in December 2024. The Group-wide external financing framework also consists of further bilateral credit facilities, including for guarantee lines.

Assets

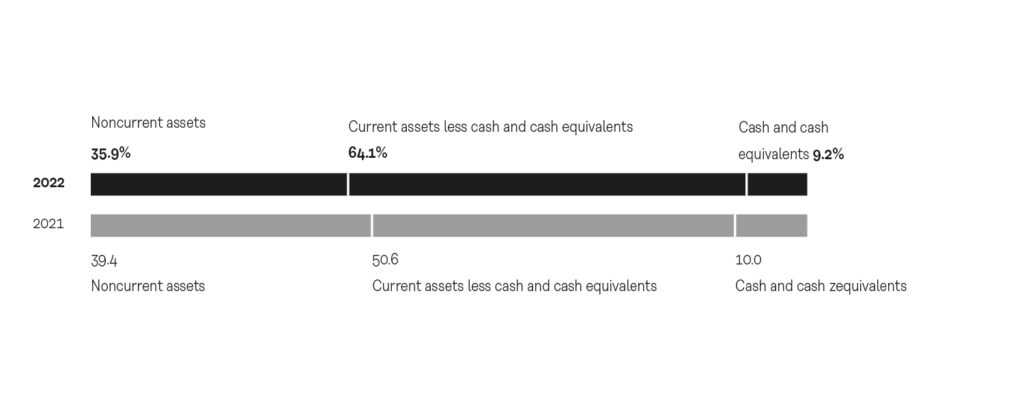

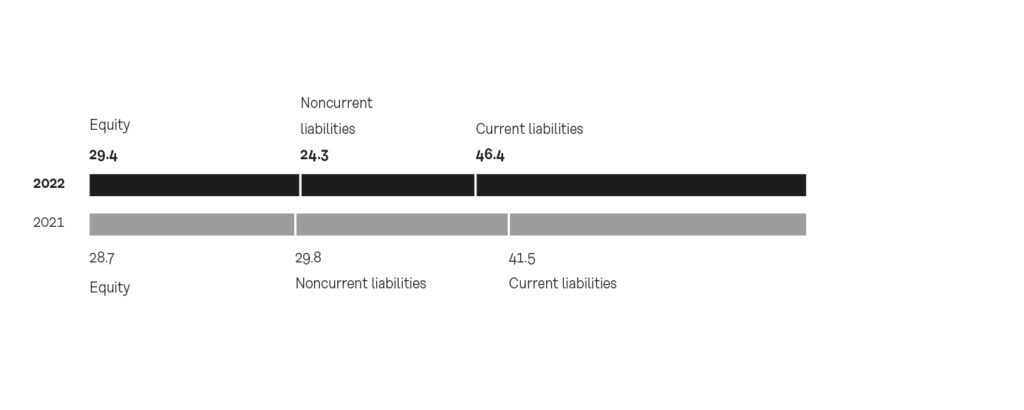

The increase in equity to €422.8m and in the equity ratio to 29.2% (31 December 2021: €369.4m and 28.7%, respectively) was mainly due to the higher discount rate applied to domestic pensions and the consolidated net profit of €11.1m (31 December 2021: €14.5m). The Koenig & Bauer Group’s total assets climbed to €1,449.2m as of 31 December 2022 (previous year: €1,288.7m).

Assets

A total of €49.8m (31 December 2021: €36.5m) was spent on property, plant and equipment and intangible assets in connection with construction and IT projects in the year under review. Capital spending includes capitalised development costs of €5.1m (31 December 2021: €5.5m). This was accompanied by depreciation and amortisation expense of €40.0m (previous year: €37.9m). On balance, intangible assets and property, plant and equipment rose slightly from €387.3m to €393.6m. With financial investments and other financial receivables slightly up on the previous year, together with the acquisition of shares in Celmacch, which is reported together with all transaction costs under “Equity-accounted investments”, and lower deferred tax assets, non-current assets widened by €18.9m over the previous year to €526.5m as of 31 December 2022 (previous year: €507.6m). Current assets increased from €781.1m at the end of 2021 to €922.7m at the end of 2022. This is mainly attributable to the increase of €94.6m in inventories to €426.2m (previous year: €331.6m) as a result of higher costs in the procurement markets as well as greater stockpiling in response to the global supply chain constraints and shortages of material. Trade receivables climbed by €26.9m to €121.6m due to the volume of revenue on the reporting date 31 December 2022 (previous year: €94.7m). As of the end of the year on 31 December 2022, cash and cash equivalents increased by €2.7m to €132.2m (31 December 2021: €129.5m). At €1,439.2m, the Group’s total assets were above the figure of €1,288.7m recorded at the end of 2021.

Equity and liabilities

The increase in the discount rate for domestic pensions together with the consolidated net profit of €11.1m (31 December 2021: €14.5m) was materially responsible for the increase in equity from €369.4m at the end of 2021 to €422.8m at the end of 2022. Accordingly, the equity ratio also widened to 29.2% as of the reporting date (end of 2021: 28.7%). Provisions for retirement benefits fell by €54.5m to €86.3m as of 31 December 2022 (previous year: €140.8m) due to the aforementioned increase in the discount rate for domestic pensions from 1.5% in the previous year to 3.9% as of 31 December 2021. In total, non-current liabilities fell by €26.0m to €358.7m (previous year: €384.7m). Current liabilities increased by €133.1m over the end of 2021, coming to €667.7m (previous year: €534.6m). This was due to the increase of €39.8m in trade payables to €104.7m (previous year: €64.9m) as a result of the larger volume of incoming deliveries from suppliers. In addition, financial liabilities and other financial liabilities rose by €43.0m to €151.9m (previous year: €108.9m) mainly due to greater drawdowns of the syndicated loan. Other liabilities and income tax liabilities climbed by €47.4m to €304.5m (previous year: €257.1m) as of 31 December 2022 primarily as a result of the prepayments received.

Segment performance

In the Sheetfed segment, order intake in particular was very favourable in 2022 again thanks to higher orders for sheetfed offset presses and the postpress range. More service business also led to an increase of €61.6m to €813.5m. At the end of the year, revenue was up €29.8m, rising to €672.2m (previous year: €642.4m). With a book-to-bill ratio of 1.21 (previous year: 1.17), the order backlog widened by 32.0% to €582.9m (previous year: €441.6m). At €19.0m, EBIT fell short of the previous year’s figure of €24.0m, translating into an EBIT margin of 2.8% (previous year: 3.7%). EBIT had on balance been inflated by €8.9m in the previous year as a result of P24x restructuring provisions.

Order intake in the Digital & Webfed segment continued to recover, increasing by €21.3m to €163.6m (previous year: €142.3m), also due to strong service business. At the end of the year, revenue was up €18.4m, rising to €139.8m (previous year: €121.4m). With a book-to-bill ratio of 1.17 (previous year: 1.17), order backlog increased by 26.9%to €112.3m (previous year: €88.5m). The segment significantly reduced its negative contribution to earnings, posting EBIT of €–19.3m, down from €–38.5m in the previous year, equivalent to an EBIT margin of –13.8% (previous year: –31.7%). EBIT had on balance been adversely affected in the previous year in an amount of €6.0m by P24x restructuring provisions. With its promising business in industrial digital printing, the versatile corrugated board sector and the growing market for flexible packaging, the segment thus achieved a significant improvement in earnings.

At €392.9m as of 31 December 2022, order intake in the Special segment fell short the previous year’s figure of €430.4m by 8.7%. Orders for Coding (marking solutions for all industries) and Kammann (direct decoration of hollow bodies made of glass, plastic or metal) as well as MetalPrint (metal packaging) were higher in the year under review. Revenue climbed by €26.9m to €417.1m (previous year: €390.2m). With a book-to-bill ratio of 0.94 (previous year: 1.10), order backlog fell by 8.7% to €253.4m (previous year: €277.6m). EBIT reached €23.2m in the period under review, compared with €34.9m in the previous year. Accordingly, the EBIT margin came to 5.6%, down from 8.9% in the previous year. EBIT had on balance been inflated by €18.1m in the previous year as a result of P24x restructuring provisions.