Macroeconomic and industry conditions

Following the historic slump in the global economy in the wake of the previous year’s global Covid-19 pandemic, the International Monetary Fund (IMF) originally stated in January that it expected an economic recovery to emerge in 2021, with growth in global production of 5.5%. In April, it revised its forecast for world economic growth upwards by 0.5% due to the availability of vaccinations, the greater adaptability of the economy and measures to stimulate the economy and the labour market. This was followed in October by a further correction, this time by 0.1% downwards, in response to the spread of the highly contagious delta variant, which triggered a fourth wave of the pandemic and new restrictions in many countries. In addition, after several years of low inflation rates, prices rose at an unusually swift rate. In addition to baseline effects, the second half of the year saw large increases as the prices of fossil-based commodities triggered an increase in energy costs, while persistent supply chain constraints drove up transport costs and the prices of various consumer and industrial goods. The global economy came under renewed pressure with the emergence of the omicron variant in November. All told, the IMF assumes that global economic output grew by 5.9% in price-adjusted terms in 2021 as a whole. In the developed economies, the recovery process has not been as consistent as expected. They were particularly hit by the heightened strain on the global production networks, especially in the manufacturing sector. As a result, several countries were unable to achieve the growth targets that had been

Year-on-year gross domestic product (%)

| Country/region | 2019 | 2020 | 2021 (estimate) |

| Global | 2.8 | -3.1 | 5.9 |

| Developed economies | 1.7 | -4.5 | 5.0 |

| Eurozone | 1.5 | -6.4 | 5.2 |

| Germany | 1.0 | -4.6 | 2.7 |

| France | 1.8 | -8.0 | 6.7 |

| Italy | 0.3 | -8.9 | 6.2 |

| Spain | 2.1 | -10.8 | 4.9 |

| United Kingdom | 1.4 | -9.4 | 7.2 |

| United States | 2.3 | -3.4 | 5.6 |

| Japan | 0.0 | -4.5 | 1.6 |

| Emerging markets and developing countries | 3.7 | -2.0 | 6.5 |

| ASEAN* | 4.9 | -3.4 | 3.1 |

| Brazil | 1.4 | -3.9 | 4.7 |

| China | 6.0 | 2.3 | 8.1 |

| India** | 4.0 | -7.3 | 9.0 |

| Russia | 2.0 | -2.7 | 4.5 |

**) Fiscal year from 1 April to 31 March

The German Mechanical and Plant Engineering Association (VDMA) also raised its forecast for mechanical engineering production in Germany for 2021 several times during the year: in January 2021, it projected an increase of 4% in real terms, raising this figure to 7% in April and 10% in June, which it subsequently confirmed in October. In mid-December 2021, the VDMA revised its forecast downwards again to a price-adjusted yearon-year increase of 7% (as of February 2022, still provisional result; corrections still pending). According to revised figures of the German Federal Statistical Office, production in the machinery and plant engineering sector in Germany increased by 6.4% in real terms in 2021. This almost matches the estimate of the VDMA economists. In summary, it notes that production growth could have been significantly higher if the supply chain constraints had not placed such a damper on mechanical engineering output, as order intake had been very promising in real terms, rising by roughly 32% over the year as a whole. However, supply chains came under strong pressure from the rapid rise in demand, triggering persistent shortfalls in the availability of intermediate products and raw materials. These were particularly pronounced in the case of electronic components and metal products. Logistics bottlenecks are exacerbating the supply chain constraints even further, for example due to the lack of euro pallets and containers. Temporary pandemic-related port closures, such as in China, also had a negative impact. All told, revenue from mechanical and plant engineering sales climbed by 6.6% in price-adjusted terms. In the printing press sector, order intake rose by a price-adjusted year-on-year rate of 22.5% in 2021. Growth of 7.1% was registered in the fourth quarter. Revenue climbed by 4.9% year-on-year in price-adjusted terms but fell short of the same quarter of the previous year by 1.8% in the fourth quarter.

The first few months of 2022 continue to be dominated worldwide by the Covid-19 pandemic, the conflict between Russia and Ukraine, the protracted delivery shortfalls and the related increase in the cost of materials as well as reduced transport capacity and increased energy costs.

Business performance

Overall statement on business performance

With its international orientation and large export quota, the Koenig & Bauer Group’s business performance in 2021 was influenced by the impact of and uncertainty arising from the global Covid-19 pandemic. Additionalstrain came from supply chain constraints and, resulting from this, the increase in the price of materials as well as insufficient transport capacities. The Koenig & Bauer Group took extensive measures at an early stage to prepare for the challenging conditions, offering tests and vaccinations at its sites in the interests of ensuring a safe working environment and to simplify the necessary business travel by employees. Despite local restrictions, production, which is based solely in Europe, was maintained and the spare parts depots in Europe, Asia and the United States remained in operation, with warehoused parts dispatched to destinations around the world every day. However, the travel restrictions impeded the worldwide deployment of Koenig & Bauer assembly staff and service technicians in view of the spread of the pandemic. For this reason, modern remote maintenance technology is of particular importance in a pandemic. Thanks to “Visual ServiceSupport”, the Koenig & Bauer Group is available to its customers around the clock and is able to resolve more than 80% of customer service queries quickly and easily without the physical presence of the service technician. The measures introduced in the previous year to maintain delivery and service capabilities as well as supplies of spare parts were duly continued and stepped up in response to the ongoing delivery shortfalls for key input products as well as low transport capacities. Koenig & Bauer announced a moderate price adjustment for its entire product range in May due to the reduced availability of raw materials.

The final quarter increasingly came under pressure from the coronavirus delta variant, the slowing vaccination rates and the emergence of the new omicron variant in November. In addition, it became evident that the global material and capacity constraints were set to be more extensive and protracted than originally expected, hampering global industrial production. Moreover, energy costs rose sharply in the fourth quarter, and here as well there is no end in sight.

In 2021, the Company worked successfully on the P24x efficiency programme, which had been adopted in September 2020. Provisions were recognised in 2020 through profit and loss for the short-term and medium term non-recurring costs of €57.6m for personnel measures required for this and reduced by roughly €23m net in 2021 due to the progress made in reaching the personnel targets. Koenig & Bauer assumed that 30% of the gross savings defined would be achieved in the year under review, adding more than €100m to Group earnings. This target was already achieved after nine months, with savings reaching roughly €31m. At around €46m as of 31 December 2021, they were significantly higher than in the previous year. This was particularly spurred by measures aimed at boosting the Group’s productivity as well as adjustments to capacities and lower quality assurance expenses. Sustainable savings were generated through cost reductions in sales and service activities and by merging the design and service departments of several business units. Furthermore, successful negotiations with suppliers and optimised discounts resulted in significant purchasing benefits, which also fundamentally offset the current price increases.

In addition to strict cost and investment management through improvements to working capital and cash flow, liquidity preservation was also a key priority. In response to the capacity utilisation shortfalls, short-time working was also introduced at various locations from 1 January 2021 – albeit to a lesser extent than in the previous year – in addition to the use of flexible working hours. To strengthen the Group’s stability and strategic flexibility, the Company obtained a flexibly repayable KfW loan of up to €120m in November 2020 to supplement the existing syndicated credit facilities. As no dividend distributions are permitted during the term of the KfW loan, the Management Board and the Supervisory Board will be proposing to the Annual General Meeting that the net profit achieved by the holding company Koenig & Bauer AG be retained. For this reason, the Company aims to discharge the KfW loan as quickly as possible so that dividend distributions can be resumed. Financially, the Koenig & Bauer Group is well positioned with a Group equity ratio of roughly 29% and more than €250m in freely available cash and cash equivalents. This was also aided by active net working capital management in the year under review.

At the end of November 2021, the Koenig & Bauer Group announced its “Exceeding Print” strategy, which is aimed at driving forward its transformation from a traditional mechanical engineering company into an agile technology group. The path that it has already embarked upon is leading to greater digitalisation and modularity, resulting in additional economic success in its core markets, especially packaging printing. Printing processes are using less material and energy, thus becoming more sustainable. In addition, Koenig & Bauer is setting itself further sustainability goals with its new “Exceeding Print” corporate strategy.

Operating earnings continued to improve from quarter to quarter in 2021. At €806.8m at the end of December, the order backlog was high, also compared to previous years. At the level of the individual segments, the recovery was particularly evident from the first quarter with strong order intake in the Sheetfed segment. This was followed in June by MetalPrint, which is part of the Special segment and registered one of the best order intakes in its history. Securities business, which forms part the Special segment, also bounced back in the third quarter with strong order intake. Starting in the third quarter, the Digital & Webfed segment showed signs of recovery, which strengthened in the fourth quarter.

In 2021, the Bauer & Koenig Bauer Group generated revenue of €1,115.8m (previous year: €1,028.6m) and consolidated earnings before interest and taxes (EBIT) of €28.5m (previous year: €-67.9m), translating into an EBIT margin of 2.6% (previous year: -6.6%). The segments contributed the following EBIT in 2021: Sheetfed €24.0m (2020: €-27.8m); Digital & Webfed €-38.5m (2020: €-25.5m), Special €34.9m (2020: €-31.8m). Group revenue thus increased by a rate within the expected range of 7-10%, rising to €1,100-1,135m, with the EBIT margin exceeding the Company’s own forecast of 2.0%. The Sheetfed and Special segments made a disproportionately strong contribution to this improvement in earnings, while the earnings contribution made by the Digital & Webfed segment was smaller.

With the publication of the figures for the second quarter of 2021, the original forecast was fleshed out in greater detail. It assumed slight organic revenue growth of 4.0% to €1,070m and balanced EBIT but did not include the effects of the adjustment to the restructuring provisions for P24x.

To summarise, the Koenig & Bauer Group’s business performance and business situation in 2021 were better than expected in the light of the effects of the Covid-19 pandemic, the supply chain constraints and, resulting from these, higher material prices and shortfalls in transport capacity.

Earnings

Roughly 32% increase in Group order intake

Order intake gradually returned to pre-crisis levels over the course of the year. At €1,290.6m as of 31 December 2021, Group orders exceeded the previous year’s figure of €974.7m by 32.4% and were thus above the industry trend for printing presses of 22.5%. In the fourth quarter of 2021, new orders increased by 19.1% to €312.0m, thus substantially outpacing the industry-wide growth rate for October – December 2021 of 7.1%.

Group order intake

| in €m | 2020 | 2021 |

| Sheetfed | 594.6 | 751.9 |

| Digital & Webfed | 109.0 | 142.3 |

| Special | 306.1 | 430.4 |

| Reconciliation | -35.0 | -34.0 |

| Total | 974.7 | 1,290.6 |

Group revenue up roughly 9% on the previous year

At €1,115.8m, Group revenue for the year ending 31 December 2021 was up 8.5% on the previous year (31 December 2020: €1,028.6m) despite the protracted pandemic-related restrictions. This exceeded the industry-wide increase of 4.9% in revenues from printing presses registered by VDMA. Revenue increased from quarter to quarter, reaching €328.4m in the fourth quarter. This was 24.3% up on the good quarter of the previous year (€264.1m) and easily exceeded the negative industry average of -1.8%.

Group revenue

| in €m | 2020 | 2021 |

| Sheetfed | 555.6 | 642.4 |

| Digital & Webfed | 128.9 | 121.4 |

| Special | 377.3 | 390.2 |

| Reconciliation | -33.2 | -38.2 |

| Total | 1,028.6 | 1,115.8 |

Nearly 30% of the Group’s revenue was achieved from service business. This means that the target of 30% was also reached on the basis of higher new press business than in the previous year.

Group revenue by product group

| in €m | 2020 | 2021 |

| Service | 301.2 | 329.8 |

| Machines | 717.6 | 774.3 |

The Group export ratio widened from 84.6% to 86.2%, with the proportion of business coming from Latin America and Africa growing substantially to 11.8% (previous year: 8.8%), while Asia/Pacific also accounted for a higher share of 26.0% (previous year: 24.8%). The share of revenue coming from Germany (13.8%), Europe excluding Germany (32.6%) and North America (15.8%) was down on the previous year (15.4%, 32.9% and 18.1%, respectively).

Geographical breakdown of revenue

| in €m | 2020 | 2021 |

| Germany | 158.7 | 153.8 |

| Rest of Europe | 338.2 | 364.4 |

| North America | 185.9 | 176.7 |

| Asia/Pacific | 255.2 | 289.6 |

| Africa/Latin America | 90.6 | 131.3 |

| Total | 1,028.6 | 1,115.8 |

| in % | ||

| Germany | 15.4 | 13.8 |

| Rest of Europe | 32.9 | 32.6 |

| North America | 18.1 | 15.8 |

| Asia/Pacific | 24.8 | 26.0 |

| Africa/Latin America | 8.8 | 11.8 |

After a roughly 30% increase, order backlog high

At €806.8m as of 31 December 2021, order backlog was up 27.7% on the previous year’s figure of €632.0m, thus reaching a high level compared with earlier years and forming a solid basis for 2022.

Group order backlog

| in €m | 2020 | 2021 |

| Sheetfed | 332.1 | 441.6 |

| Digital & Webfed | 67.6 | 88.5 |

| Special | 237.4 | 277.6 |

| Reconciliation | -5.1 | -0.9 |

| Total | 632.0 | 806.8 |

Earnings improved

Despite the ongoing pandemic in 2021 and a challenging procurement environment, earnings improved thanks to the swifter emergence of the savings effects under the P24x efficiency programme and the more efficient implementation of the related personnel measures. Earnings in the individual segments improved at different points in time, as each segment reacted differently to the pandemic as well as the supply chain constraints and the resultant increases in the prices of materials. Non-recurring effects in 2021 with an impact on the Group’s business performance arose from adjustments of around €23m net to the restructuring provisions for the P24x efficiency programme. In the previous year, non-recurring effects had amounted to around €-49m with a corresponding effect on the Group’s earnings. Service business, whose share in revenue widened to 29.6% (previous year: 29.3%) despite the decline in Digital & Webfed, is the Group’s main source of revenue. With the P24x efficiency programme, we are working intensely on improving earnings from new press business as well. The “Exceeding Print” strategy is focusing on our strengths and thus also vigorously pursuing the goal of permanently widening the share of service business in Group revenue to 30%.

EBIT margin of 2.6% achieved

Despite the pandemic, reduced short-time working and positive volume and mix effects, gross profit increased by 48.4% in 2021 to €298.1m (2020: €200.9m) thanks to lower production costs among other things. Reflecting this, the gross margin widened to 26.7% (2020: 19.5%). At €46.7m, R&D expenses were up on the previous year’s figure of €39.1m. Selling expenses increased slightly by €1.4m to €131.1m. Administration expenses fell by €6.3m to €88.4m in the same period. Net other expenses came to €-4.4m, compared with €-6.9m in the previous year.

Accordingly, EBIT reached €28.5m in 2021 (2020: €-67.9m). The improvement of €96.4m over the previous year is mainly due to the more efficient implementation of the P24x personnel measures despite the lower use of short-time work (roughly €22m), positive volume and mix effects (roughly €1.2m) in spite of the increase in the cost of materials in the high single-digit million euros and the cumulative non-recurring effects arising in the previous year (roughly €49m). This is also reflected in the adjustment of the restructuring provisions for the efficiency programme (roughly €23m net) and the P24x savings effects (roughly €46m). In particular, Koenig & Bauer succeeded in replacing the cost-reduction effects from the use of short-time working in the previous year with long-term and sustainable measures under P24x. Consequently, the EBIT margin improved from -6.6% to 2.6% in 2021. Adjusted for the changes to the P24x restructuring provisions, EBIT came to €5.7m; adjusted for the accumulated non-recurring effects, EBIT had equalled €-18.9m in the previous year. EBIT reached €11.8m in the fourth quarter (2020: €6.2m), thus marking a further sequential improvement to earnings in the year under review.

The interest result of €-9.5m (2019: €-5.6m) led to earnings before taxes (EBT) of €19.0m, compared with €-73.5m in the previous year. Income taxes amounted to €4.5m (previous year: €29.6m). The higher tax expense in the previous year is primarily due to impairments of deferred tax assets on unused tax losses, which were not considered to be recoverable for the purposes of the preparation of a new integrated five-year plan. At €14.5m (previous year: €-103.1m), Group net profit translates into earnings per share of €0.83 in 2021 (previous year: €-6.27).

Group income statement

| in €m | 2020 | 2021 |

| Revenue | 1,028.6 | 1,115.8 |

| Cost of sales | -827.7 | -817.7 |

| Gross profit | 200.9 | 298.1 |

| Research and development costs | -39.1 | -46.7 |

| Distribution costs | -129.7 | -131.1 |

| Administrative expenses | -94.7 | -88.4 |

| Other operating income/expenses | -6.9 | -4.4 |

| Impairment gains and losses on financial assets | 1.6 | 0.9 |

| Other financial results | – | 0.1 |

| Earnings before interest and taxes (EBIT) | -67.9 | 28.5 |

| Interest result | -5.6 | -9.5 |

| Earnings before taxes (EBT) | -73.5 | 19.0 |

| Income tax expense | -29.6 | -4.5 |

| Net profit | -103.1 | 14.5 |

| Earnings per share | -6.27 | 0.83 |

| % of revenue | 2020 | 2021 |

| Cost of sales | -80.5 | -73.3 |

| Research and development costs | -3.8 | -4.2 |

| Distribution costs | -12.6 | -11.7 |

| Administrative expenses | -9.2 | -7.9 |

| Other income/expenses | -0.6 | -0.4 |

| Interest result | -0.5 | -0.9 |

| Income taxes | -2.9 | -0.4 |

| Net profit | -10.0 | 1.3 |

Finances

Substantial improvement in cash flow from operating activities and in free cash flow; net financial debt reduced

Cash flow from operating activities improved significantly, rising to €95.0m in the period under review, compared with €12.2m in the previous year. Cash flow from investing activities came to €-38.7m (31 December 2020: €-36.3m). Free cash flow also improved substantially, widening from €-24.1 in the previous year to €56.3m. The increase of €80.4m was materially underpinned by the reduction in net working capital from €344.0m as of 31 December 2020 to €297.1m. Cash flow from financing activities came to €-68.4m (31 December 2020: €-25.0m) due to the partial repayment of the syndicated loan of €60.0m. At the end of December 2021, cash and cash equivalents stood at €129.5m (31 December 2020: €137.8m), with freely available liquid funds exceeding €250m. Adjusted for bank liabilities of €126.6m, net financial debt improved substantially by €50.0m to €2.9m (31 December 2020: €-47.1m). The Group has access to syndicated credit facilities of a total of €400m from a consortium of excellent banks. The syndicated finance, which consists of a guarantee credit facility and a revolving credit facility of €200m each, has a term expiring in December 2024. Against the backdrop of the Covid-19 pandemic and the related funding programmes, Koenig & Bauer was also able to reach an agreement with KfW and the syndicate banks in 2020 to increase the revolving credit facility by €120m on standard market terms in order to ensure the Company’s economic stability. This adjusted facility also has a term expiring in December 2024. The Group-wide external financing framework also consists of further bilateral credit facilities, including for guarantee lines.

Assets

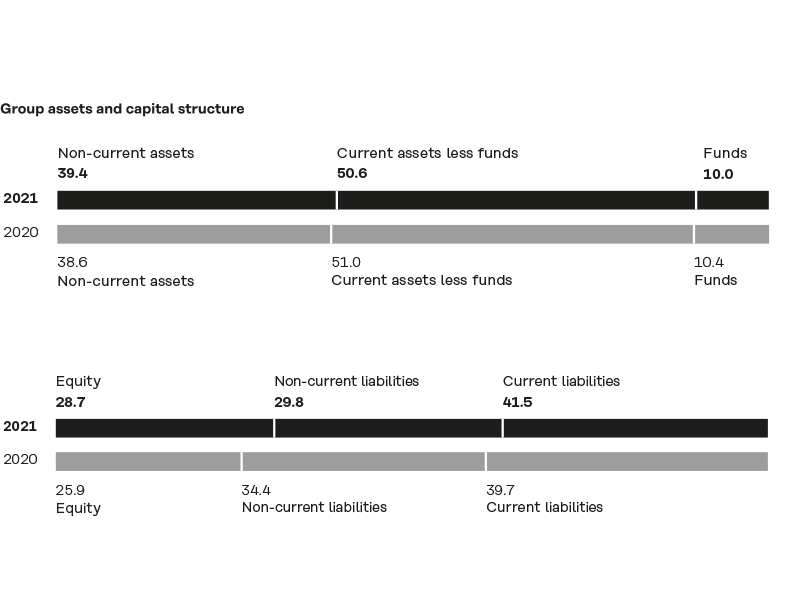

Increase in equity ratio to roughly 29.0%

The consolidated net profit of €14.5m (31 December 2020: consolidated net loss of €103.1m) contributed significantly to the increase in equity to €369.4m and in the equity ratio to 28.7% (31 December 2020: €342.2m and 25.9%, respectively). The Koenig & Bauer Group’s balance sheet total fell to €1,288.7m as of 31 December 2021, down €32.4m on the previous year’s figure of €1,321.1m.

Assets: net working capital reduced

36.5m (31 December 2020: €46.5m) was spent on property, plant and equipment and intangible assets in connection with construction and IT projects in the period under review. Capital spending includes capitalised development costs of €5.5m (31 December 2020: €11.8m). This was accompanied by depreciation and amortisation expense of €37.9m (previous year: €34.5m). On balance, intangible assets and property, plant and equipment dropped slightly from €392.3m to €387.3m. With financial investments and other financial receivables up slightly on the previous year accompanied by somewhat higher deferred tax assets, non-current assets came to €507.6m and were virtually unchanged over the previous year’s figure of €509.7m. Current assets decreased by €30.3m to €781.1m, down from €811.4m in the previous year. This was mainly due to the decline of €26.0m in inventories to €331.6m (31 December 2020: €357.6m). As of the end of the year on 31 December 2021, cash and cash equivalents were down €8.3m, standing at €129.5m (31 December 2020: €137.8m). As a result, net working capital fell by €46.9m to €297.1m as of 31 December 2021 (31 December 2020: €344.0m).

Equity and liabilities: net financial debt down over the previous year

The Koenig & Bauer Group’s equity rose to €369.4m as of 31 December Provisions for retirement benefits and similar obligations dropped to €140.8m as of 31 December 2021 (31 December 2020: €165.6m) mainly due to the increase in the discount rate for domestic retirement benefits from 0.9% as of 31 December 2020 to 1.5%. Non-current other provisions rose by €7.6m to €47.9m (31 December 2020: €40.3m). By contrast, non-current financial liabilities and other financial liabilities were reduced by €52.0m to €117.6m as of the reporting date, mainly due to the repayment of the syndicated loan of €60.0m (31 December 2020: €169.6m). Overall, this resulted in a reduction in non-current liabilities of €69.3m to €384.7m as of 31 December 2021 (31 December 2020: €454.0m).

On the other hand, current liabilities rose slightly by €9.7m to €534.6m (31 December 2020: €524.9m). Current other provisions fell by €21.1m, mainly due to the partial adjustment of around €23m net to the P24x restructuring provisions to €103.7m (31 December 2020: €124.8m). This was offset by an increase of €29.4m in current other liabilities to €251.2m (31 December 2020: €221.8m) as a result of higher liabilities from other taxes.

Segment performance

Sheetfed consistently up on the previous year

In the Sheetfed segment, order intake in particular was very favourable in 2021 thanks to higher orders for sheetfed offset presses and the post-press range. More service orders also led to an increase of 26.5% to €751.9m, which was above the industry average for printing presses of 22.5% (previous year: €594.6m). At the end of the year, revenue was up 15.6%, rising to €642.4m (previous year: €555.6m) and thus significantly exceeding the industry-wide growth of 4.9% registered by VDMA. With the book-to-bill ratio standing at 1.17 (previous year: 1.07), the order backlog rose from €332.1m to a historical high of €441.6m as of 31 December 2021. EBIT increased by €51.8m to €24.0m, translating into an EBIT margin of 3.7% (previous year: -5.0%). The adjustment to the P24x restructuring provisions had a positive impact of €8.9m on EBIT.

Digital & Webfed showing signs of a recovery in order intake in the second half of the year

Order intake in the Digital & Webfed segment was still heavily burdened by pandemic-related spending restraint in the first half of the year but increased cumulatively by 30.6% to €142.3m (previous year: €109.0m), thus exceeding the industry average of 22.5%. In addition to more service orders, higher orders for corrugated board printing presses (Corru family), web digital printing with RotaJET presses, HP presses and flexible packaging printing resulted in an increase, especially in the fourth quarter. Orders for web offset presses moved in the opposite direction. At €121.4m, revenue was slightly down on the previous year’s figure of €128.9m. Order backlog increased by 30.9% to €88.5m as of 31 December 2021 (previous year: €67.6m). In addition to customers’ pandemic-related purchasing restraint, EBIT was still impacted by start-up costs and investments in further product development, reaching €-38.5m (previous year: €-25.5m). Accordingly, the EBIT margin came to -31.7%, compared with -19.8% in the previous year. The adjustment to the P24x restructuring provisions had a negative impact of €6.0m on EBIT.

Special with a roughly 40% increase in new orders

At €430.4m as of 31 December 2021, order intake in the Special segment exceeded the previous year’s figure of €306.1m by 40.6%. This also exceeded the industry-wide average increase of 22.5% registered by VDMA. The growth in orders was also underpinned by a greater number of service orders from all businesses. Revenue grew by 3.4% from €377.3m in the previous year to €390.2m. At €277.6m, the order backlog as of the end of the year was up 16.9% on the previous year’s figure of €237.4m. In the period under review, EBIT increased by €66.7m to €34.9m (previous year: €-31.8m), mainly driven by a strong final quarter. Accordingly, the EBIT margin reached 8.9%, up from -8.4% in the previous year. The adjustment to the P24x restructuring provisions had a positive impact of €18.1m on EBIT.